Guinea has record growth projections of 8.7% in 2026, 9.3% in 2027 according to the IMF[i], driven by the Simandou mining mega-project. But this macro-financial dynamic alone does not guarantee inclusive human development or environmental sustainability. The question is no longer to choose between growth and ecology, it is to integrate sustainable finance at the heart of public policies. The mining boom is propelled our country among the most vibrant economies in the world. Inflation stabilizes at 4.1%, the current deficit narrows dramatically, from -22.3% of GDP in 2025 to almost balance in 2027, and the debt-to-GDP ratio fell by 48.1% to 44.7%. A rare macroeconomic trajectory in West Africa. However, with a HDI ranked 179th in the world and 43.7% of the population below the poverty line, Guinea embodies the « paradox of abundance« . A country that owns two-thirds of the world’s bauxite reserves, the largest unexploited iron deposit in the world (3.3 billion tons in Simandou), a hydroelectric potential of more than 6,000 MW and the sources of several major rivers in West Africa. Contemporary globalization is marked by a planetary awareness. Environmental externalities can no longer be ignored. Sustainable finance, which integrates Environmental, Social and Governance (ESG) criteria in allocation decisions, has become a requirement. Since the Paris Agreement (2015), international capital flows now systematically include environmental parameters in their allocation criteria. The European green taxonomy, the International Sustainability Standards Board (ISSB) and the requirements of the Bretton Woods institutions redefine the conditions for access to international funding.

In 2025, the global outstanding amount of green, social and sustainable bonds exceeded USD 4 trillion. Africa, although marginal (less than 2%), is beginning to capture these flows. In this context, countries rich in natural resources, like ours, are faced with a double injunction. Exploit their resources to finance development, while complying with sustainability standards that condition foreign direct investment. However, this rapid economic take-off is accompanied by a triple vulnerability: climate, social and environmental. The challenge is therefore no longer to choose between growth and sustainability, but to integrate sustainable finance into budget planning via rigorous extra-financial indicators. This is the subject of this first article.

The imperative of climate-sensitive budgeting

Guinea is at a structural inflection point. Its growth model, driven by the extractive sectors (bauxite, iron ore, gold) and hydroelectricity, remains strongly exposed to climatic hazards. Rainfall variability, coastal erosion, accelerated deforestation and intensification of extreme events directly threaten the productive base, food security and the viability of energy infrastructure.

In this context, climate-sensitive budgeting (or green budgeting) is a macro-fiscal imperative. According to the ND-GAIN Index, the country has a high structural vulnerability, aggravated by a level of readiness that is still too low, which reduces its ability to absorb and recover from climatic hazards. Macroeconomic projections are alarming. Rainfall variations and thermal shocks could reduce real GDP by 11.6% by 2050 and reduce agricultural productivity by 25%.

Climate shocks generate tax scissor effects: decrease in revenues (slowdown in agriculture, mining interruptions, decrease in hydroelectric production) and increase in spending (reconstruction, food imports, social nets). Without climate labeling and climate stress tests integrated into the Debt Sustainability Analysis (DSA), Guinea risks underestimating contingent liabilities and genering structural deficits. The IMF points out that the absence of climate-adjusted tax rules reduces budgetary room for manoeuvre and increases the likelihood of distress.

Guinea is mobilizing significant funding for infrastructure (roads, dams, mining networks). However, an investment not aligned with climate trajectories exposes the country to the risk of stranded assets and a depreciation of public capital. The Climate-PIMA (Public Investment Management Assessment) tool developed jointly by the IMF and the World Bank shows that the integration of climate criteria in the selection, monitoring and evaluation of projects increases the social and financial return of expenditure, while protecting the budget space in the medium term.

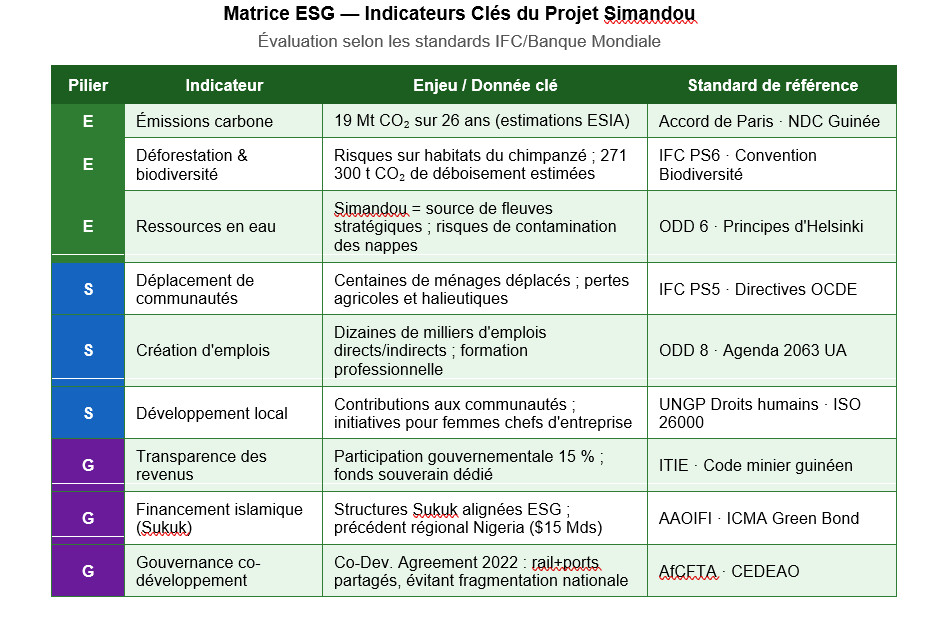

Simandou under the ESG prism: the full-size test

With $20 to $23 billion in investment, 600 km of railway track and a deep-water port in Morebaya, Simandou is the continent’s largest mining and infrastructure project. Since December 2025, the first loads of ore have left Guinean soil. Two consortia operate the deposit, with a government stake of 15% in each, a capital strategic asset. ESG performance is now directly linked to access to international financing. Rio Tinto submitted environmental and social impact assessments, redesigned its mining plan to protect chimpanzee habitats, and committed to a « Simandou 2040 » roadmap integrating vocational training, environmental protection and climate resilience. The table below lists the key indicators:

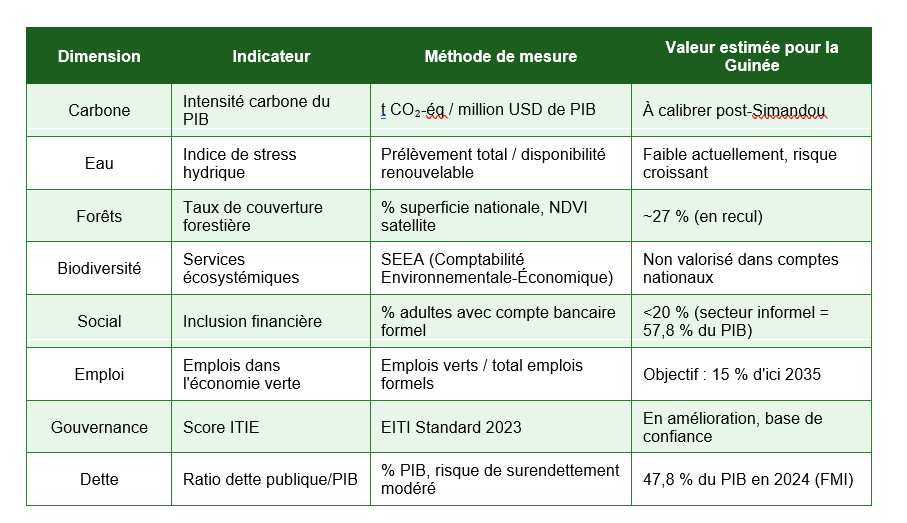

Integrate extra-financial indicators into the national budget

With structurally low tax revenues (14% of GDP in 2023 compared to a potential of 20%) and a budget deficit of 3.1% in 2024, Guinea cannot manage its transformation by traditional financial aggregates alone. Traditional budget planning, centered on financial aggregates (GDP, tax revenues, budget deficit), is insufficient for an economy like Guinea, which manages exceptional natural heritage and systemic environmental risks. The Bretton Woods institutions advocate the integration of extra-financial indicators in medium-term spending frameworks. Here are the priorities:

Green digital: an opportunity to seize

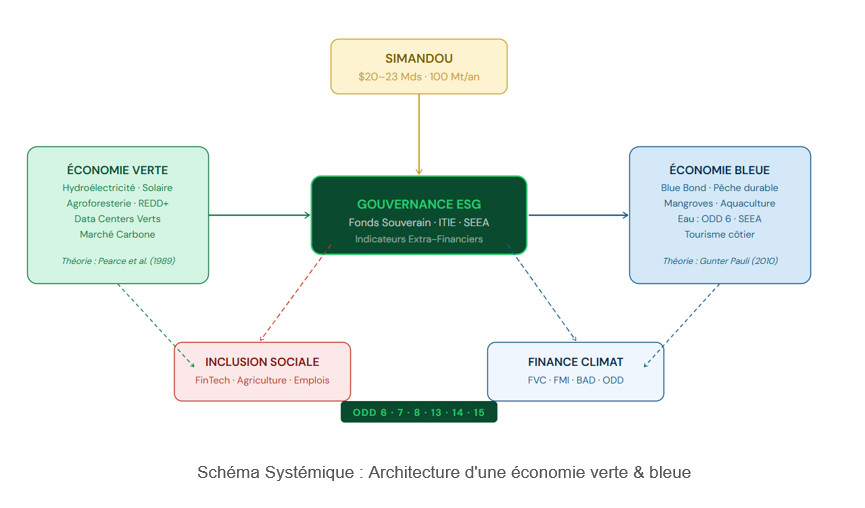

The African data center market is expected to triple to exceed $3 billion by 2030 (WEF). But a conventional data center consumes as much electricity as a city of 25,000 inhabitants, an unsustainable burden in a country where only 47.7% of households have access to electricity. Guinea has two unique assets, a hydroelectric potential of more than 6,000 MW (less than 10% exploited) and a strategic position on Atlantic submarine cables (2Africa, Equiano). A green data center in Conakry or Kindia, powered by the Souapiti (450 MW) and Kaléta (240 MW) dams, would offer an almost zero carbon footprint and environmental monitoring services for Simandou, all with maximum ESG attractiveness for impact investors.

Water and the forest: assets to be valued

Water is the most undervalued strategic asset. The country is the source of several major West African rivers, and has a hydroelectric potential of 6,000 MW of which less than 10% is exploited. The Kaléta dam (240 MW, inaugurated 2015) and that of Souapiti (450 MW) represent the first valuations of this blue capital, but they are facing increasing droughts that reduce their productivity. Guinea is the « water tower of West Africa », source of Senegal, Niger, Gambia. Its forests (27% of the territory, in decline), its coastal mangroves and its peat bogs give it considerable potential in carbon finance (REDD+, Blue Carbon). REDD+ credits are traded between $5 and $30 per ton of CO2 in voluntary markets.

However, with only 71% of households having access to water in 2022, and Simandou mines threatening watersheds that supply tens of millions of people in the sub-region, water governance is a national and regional security imperative. Its accounting valuation remains absent from the national accounts, this is a gap to be filled.

The development of sovereign blue bonds, on the model of the Seychelles that we analyze below, would allow Guinea to finance the protection of its watersheds and coastal mangroves, while reducing its dependence on traditional concessional financing. The African Union, through its Strategy for the Blue Economy (2019), offers a continental framework for this approach.

Two inspiring African models

Morocco: Solar energy as a lever for development

The Noor Ouarzazate solar complex (580 MW, the world’s largest concentrated solar power plant) supplies more than a million Moroccans and compensates for about 690,000 tons of CO2 per year. Morocco aims for 52% renewable electricity capacity by 2030, and has established itself as the most attractive clean energy investment market in Africa and the Middle East in 2022. Lesson for Guinea, a dedicated agency, green bonds backed by concrete assets, and an integrated social plan, three ingredients that can be transferred to the Guinean hydroelectric sector.

Seychelles: The world’s first sovereign Blue Bond

In 2018, the Seychelles issued the world’s first sovereign Blue Bond ($15 million) to finance sustainable fishing and marine conservation. Result: 30% of protected national waters, more than 600 jobs created, and a 10 to 15% increase in artisanal catches. This model has helped grow the global Blue Bond market to $15.25 billion. The Guinean Atlantic façade, its mangroves and fishing resources form the natural basis of such an instrument.

Eight recommendations for a green & blue Guinea

- Create a Green and Blue Sovereign Fund of Guinea (FSVBG) backed by Simandou’s revenues, allocating at least 30% to green and blue investments, with ITIE governance.

- Issue a sovereign Blue Bond of $50–100 million (with IFC/World Bank support) to protect watersheds, restore mangroves and develop sustainable fishing.

- Integrate natural capital accounting (SEAS/UN) into national accounts to enhance forests, water and biodiversity and access REDD+ financing.

- Impose a binding ESG framework (annual ISSB/GRI reports, environmental guarantee, internal carbon pricing) on any mining project exceeding $100 million.

- Develop a national strategy for green hydroelectric data centers, certified by ISO 50001, in the service of digital inclusion and environmental monitoring.

- Create a national register of REDD+ carbon credits connected to international voluntary markets (Gold Standard, Verra), aiming at 5 to 15 million credits per year.

- Adopt a National Blue Economy Strategy (SNEB) covering sustainable fishing, aquaculture, coastal tourism, mangroves and cross-border management of river basins.

- Include Guinea in the international climate financing mechanisms (REDD+, Green Climate Fund, IMF Facility for Resilience and Sustainability).

A historic opening of opportunity

At the end of this reflection, it must be noted that Guinea is at a strategic crossroads. Long captive of rent growth, supported almost exclusively by the exploitation of bauxite and a few export crops, the country has suffered the limits of a model that is both volatile, extractive and vulnerable to exogenous shocks. However, its untapped potential of dense forests, stream rashes, seafront of more than 300 km, mangroves, water and solar deposits, draws the contours of a completely different trajectory. Daring the green and blue economy is therefore not a luxury of a developed country, but a boost to economic survival and structural catch-up. The cost-benefit analysis, in the light of the models evaluated by the World Bank, is unequivocal. In the medium term (5 to 7 years), every dollar invested in mangrove restoration, sustainable fishing, decentralized solar energy or climate-intelligent agriculture generates an economic return higher than that of conventional extractive activities, once the hidden costs of environmental degradation are integrated (loss of soil productivity, health costs, coastal erosion). Guinea can thus avoid the trap of the environmental « resource curse« , where natural abundance turns into collective impoverishment. Daring the green and blue economy means getting out of the short-term management of annuities to enter a logic of accumulation of productive natural capital.

Guinea has the rare opportunity to become a case study in West Africa, combining responsible mining development (low-footprint bauxite) and the development of an inclusive green and blue economy. Audacity today is to act before the cost of inaction becomes unsustainable.

source : le djely